Bankfeed works as an add-on for Microsoft Dynamics 365 Business Central. Therefore the usage of this ERP system is necessary. The solution works best with the three latest versions of Business Central.

Before installing Bankfeed, we recommend checking if the following conditions are met:

1. Open banking API (PSD2*) is not occupied.

If you use online payment provider services (Wordline, Wordpay, etc.), they might be connected through an open banking API. Therefore, Bankfeed will not be able to connect to this API as it is already occupied. In these situations, we can connect Bankfeed through the bank’s direct API, known as a Gateway. However, it usually requires additional banking fees and additional implementation hours.

2. Banks provide the information required for recognition and reconciliation.

Even though open banking is regulated using the PSD2 protocol and is mandatory for all EU banks, the banks treat these requirements differently. The amount of information provided through the APIs and its quality can differ depending on the bank. This can lead to a situation where Bankfeed will not be able to properly identify customers/vendors or documents because of the lack of data.

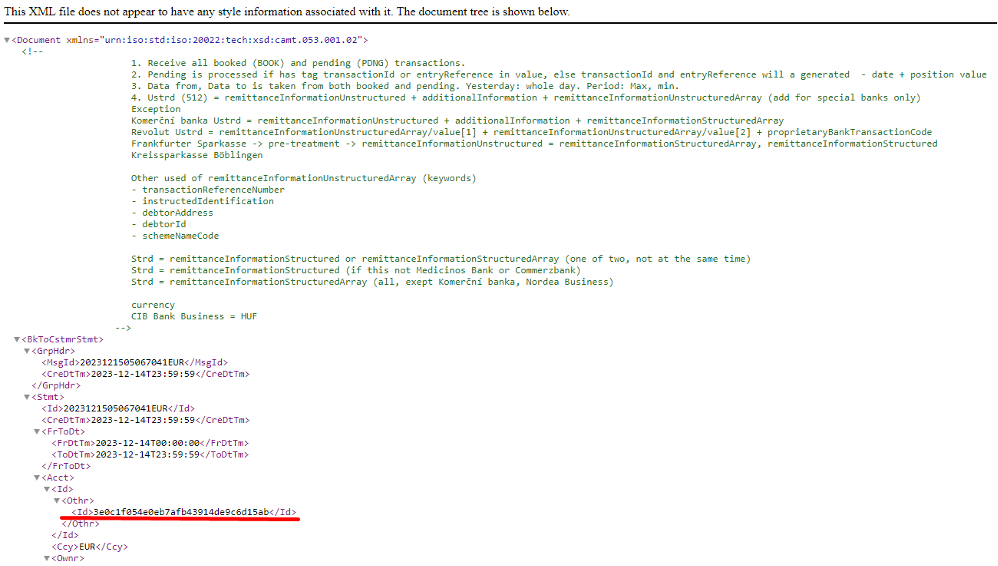

Here is a list of mandatory bank fields needed to enable Bankfeed’s payment recognition and reconciliation. Please check HERE if the banks you are using provide the information from these fields:

- creditorAccount – customer recognition by IBAN

- creditorId – customer recognition by ID

- creditorName – customer name comparison when the document is identified

- debtorAccount – vendor recognition by IBAN

- debtorName – vendor name comparison when the document is identified

- endToEndId – document Nos to identify

- entryReference – document Nos to identify

- remittanceInformationStructured – document Nos to identify

- remittanceInformationStructuredArray – document Nos to identify

- remittanceInformationUnstructured- document Nos to identify

- remittanceInformationUnstructuredArray- document Nos to identify

*The Revised Payment Services Directive (PSD2) is a set of laws and regulations for payment services in the European Union (EU) and the European Economic Area (EEA). Under this payment services directive, banks and other financial institutions are required to provide APIs (Application Programming Interfaces) for regulated and licensed external services providers, commonly referred to as third-party providers. This practice when banks provide APIs for third-party providers is also known as Open banking.